How Much to Pay in a Full and Final Settlement

Obviously you will want to pay as little as possible, but there are some things that you may need to know about.

Age of a Debt in a Full and Final Settlement Matters

The older the debt is, the more chance you have of getting a low or very low settlement for that debt!

Debts are often sold on for pennies in the pound when companies are unable to collect them from individuals. This is because the companies that buy the debt are generally willing to take on the risk of not being able to recover the debt from the individual in exchange for a discounted rate. The companies that buy the debt hope to make a profit from recovering the original amount in full (and some do), or at least a portion of it. This means that the companies that buy the debt can offer a fraction of the amount owed in exchange for the right to pursue the debt. This helps to reduce the risk to the original creditor and can help them to recover some of the money that they are owed. When you think that this happens a number of times with older debt, then is some cases a Debt Collection Agency (DCA) may only pay £0.05 pence in the pound or less for an older debt. So, if you are making an offer that gives them a bit of profit, they are more likely to accept.

How Much to Pay Creditors in a Full and Final Settlement

In order for you to even consider a full and final settlement, you will need access to a lump some. Often, third parties or family friends may be willing to help you out with a lump sum that is to be used in a full and final settlement. Whenever a creditor asks you where the money is, all they need to know is that the funds are held by a third party or family friend. So now lets assume that your third party or family friend is willing to set aside £10,000 for your full and final settlement.

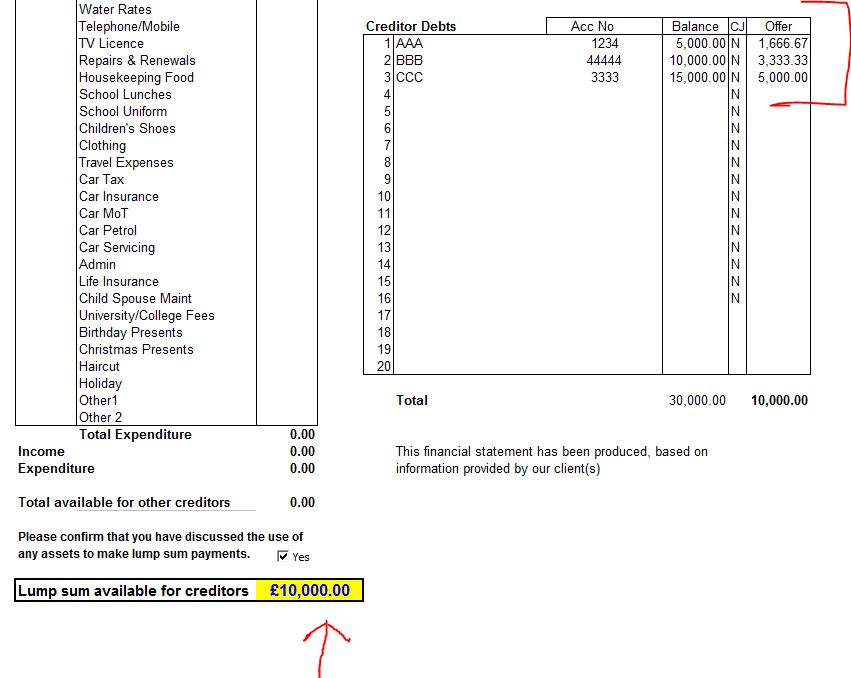

Calculating How Much to Pay Creditors on a Pro-rata Split

So, you now have £10,000 available to pay of your creditors in a full and final settlement, BUT you have £30,000 worth of debts to 3 creditors as follows:

Creditor AAA £5,000

Creditor BBB £10,000

Creditor CCC £15,000

Total Debts £30,000

So from the figures above we need to calculate the maximum amount that we can pay all the creditors fairly on a Pro-Rata Split. The amount you owe is then divided by the total debt, multiplied by the income available, giving you the monthly payment

So for creditor AAA it is calculated as follows:

£5,000 Divided by £30,000 Multiplied by £10,000 equals £1,666

That is the maximum amount you would offer to creditor AAA.

REMEMBER if you offer more to creditor AAA, then that will leave you LESS to offer creditors BBB and CCC.

Ask Your Creditor How Much they Will Accept in a Full and Final Settlement

Before you even think about making an offer to a DCA, why not just contact them and ask them how much they would accept in a full and final settlement if you can pay immediately? (get it is writing) You never know, they may well want to settle the debt quickly and get in some funds! So they may well want much less than you were thinking or willing to offer.

Getting the Best Value for Money in a Full and Final Settlement

In the calculations above, your third party or family friend has offered to stump up £10,000 to pay off you debts in a full and final settlement. However, that does not mean that you have to use the full amount being offered. You could start off by just calculating that there is only £5,000 available as a lump sum. CAUTION the lower the amount that you are willing to offer, the longer it could take for you to get a DCA to accept your offer in a full and final settlement!

Negotiate with Creditors in Writing

Full and final settlement should always be done in writing for a few reasons. First, it provides a written record of the agreement and its details. This may be useful in the event of a dispute or disagreement between the parties at a later date. Second, the written agreement serves as a reminder of the terms of the settlement, including any conditions which must be met by each party. Finally, written full and final settlements also provide clarity and assurance that the agreement will be upheld by both parties. By having the agreement in writing, each party can be held accountable to the terms of the settlement.

CAUTION: Full and Final Settlement May Not Work if You Have any Assets

Full and final settlements work best if you do not have any assets that the creditor may be aware of. So, if say for example you are a property owner and there is a substantial amount of equity in that property, then a creditor may/will reject a low offer in a full and final settlement. Why would a creditor accept a low offer, if they can come and get your home and recoup the full amount.

Full and Final Spreadsheet Pro-Rata Calculator

You can download a copy of the Full and Final Settlement Spreadsheet. When completing the spreadsheet, you should also use that to show how dire your situation is and the best result for a creditor is to accept a full and final settlement………….. Holidays etc should be zero.

Full and Final Settlement Success Stories

This site is littered with many successful full and final settlements, just click on Full and Final Settlements Results.

Pingback:Barclaycard Debt of £12,138 Settled for £3,624 with Full & Final Settlement – Johnny Debt