DIY Debt Management Plan

Can You Do Your Own Debt Management Plan

The simple answer is YES! However, to start with is may be difficult to implement. I would say that if you are going to do your own Debt Management Plan, you need to put some time aside to deal with creditors, be strong willed, and do your research! I would also recommend that you get the latest book which can be found here on Amazon Debt Advice Handbook. Although this book is rather expensive, I think that it is good value for money for all the information that it has within. It will give you a full understanding of; how the debt system works; what creditors, bailiffs, etc can and can not do, and much, much more!

How to Do Your Own Debt Management Plan

The very first thing that you need to do is get together a list of all the companies that you owe money to. If you do not have an up-to-date statement, you can write to a creditor requesting this. I would also at this stage recommend that you ALWAYS correspond with creditors in writing. This saves you more earache on the phone and also you then have written evidence immediately to hand. The information you need is; Creditor; Creditor Collection Agency Address; Account or Reference Number; Amount Outstanding.

Contact (in writing) the creditors and inform them that you are having financial difficulties and you are considering going into a Debt Management Plan or DMP. In the letter confirm that the company is still dealing with the debt and also the amount outstanding. You can also add to the letter that once you are in receipt of the information, you will be forwarding to them an in depth Income & Expenditure, with a proposed solution.

As companies want the money, you can be fairly sure that they will all write back to you!

DIY Income & Expenditure

The next thing that you will need to do is, prepare an Income & Expenditure. The information that you will require for your I&E (Income & Expenditure). Is as follows (not all may apply to you):

Monthly Income:

Wages/Salary

Additional Income

Benefits

Other Income

Monthly Expenditure:

Rent or Mortgage Payments

2nd/3rd Charges on Your Property

Buildings Contents Insurance

Council Tax

Gas and or Electric

Water Rates

Telephone Mobile

TV Licence

Housekeeping Food (this is usually calculated at £150 for the first person and £100 each other person)

School Uniforms

School Lunches

Children’s Shoes

Clothing

Travel Expenses

Car Tax

Car Insurance

Car MoT

Car Petrol

Car Servicing

Admin

Life Insurance

Child/Spouse Maintenance

University/College Fees

Birthday Presents (A creditor could question and want some or all of the funds spent on this)

Christmas Presents (A creditor could question and want some or all of the funds spent on this)

Haircut (£5 per month should cover)

Holiday (A creditor could question and want some or all of the funds spent on this)

Priority Arrears

Other

Creditor Details:

Creditor Name

Account Number

Amount Owed

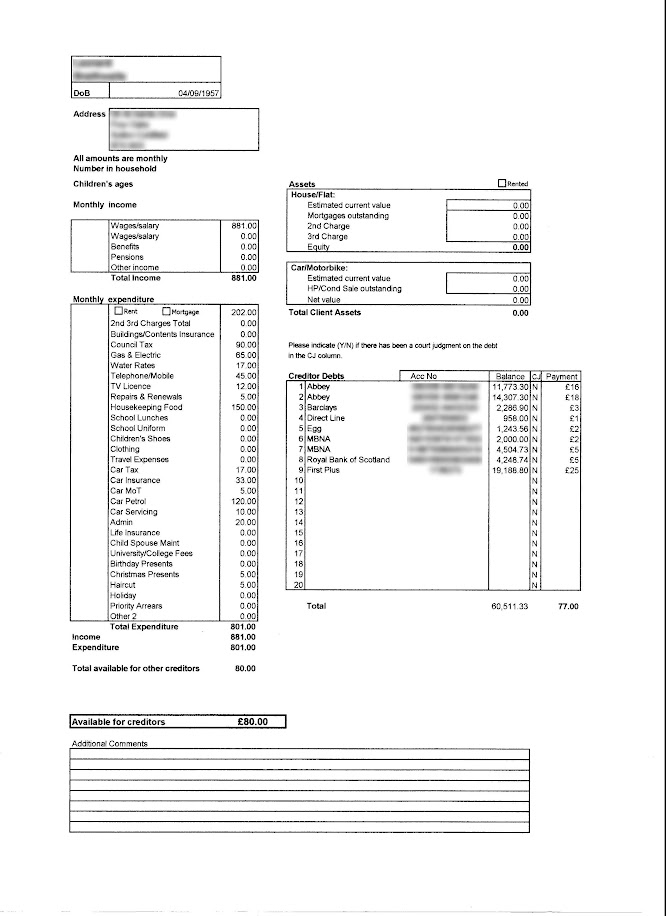

Below is an example of a completed I&E You can download on this link an actual Income and Expenditure Spreadsheet

Holidays, Christmas and Birthday Presents etc should be ZERO, as creditors may want that too!

Completing Your DIY Income & Expenditure

Now that you have your Income and Expenditure Spreadsheet, you need to complete it as best you can. This is your opportunity to show why you will need to make reduced payments. In the notes section at the bottom you can also use that to state why you are no longer able to maintain the standard monthly payments.

As you enter the figures on your spreadsheet, you will see that it will total up your Income and Expenditure. As you fill out the details of what is owed to the creditor, the spreadsheet should automatically show in the “Payments” column how much each creditor should receive on a pro-rata split. In other words this is how much money is allocated to each creditor.

This post may also be of interest to some readers What Expenses Can I Claim for If Going Bankrupt? Maybe a little out of date now, but gives you a rough idea on expenses.

Sending Your DIY Income & Expenditure to Creditors

Now that you have completed your I&E you need to send a copy to each creditor with a covering letter, informing them that you wish to go into a Debt Management Plan. Explain that they will be receiving a payment of X amount as per the pro-rata split on the income and expenditure. At the same time request from the Creditors the relevant bank account details for you to set up a Standing Order to them. Do not set up a Direct Debit with a creditor as this means you have less control , when and how much payment is made. With a Standing Order, you are in total control and can make changes to creditors if your circumstances should change again for the worse. If this happens and you need to lower your monthly payments, you will need to set up a new agreement with each creditor. Just redo the process above.

If you have the Creditors Account details you can start making immediate payments to them. This shows that you are making every effort to make payment (also known as forced payment). This way a creditor can not claim that you are not making an effort.

Request the Freezing of Interest

Another thing to consider in your letter, request that due to your current financial situation, all interest on the account is set to ZERO. Most creditors do stop adding interest, but it is always best to ask! (I respectfully request the freezing of any interest on the outstanding balance for the duration of the plan in line with section 14 of the British Banking Code.)

Dealing with Someone Else’s Debt

If you are doing a DIY DMP for someone else. Make out a form stating that you will be dealing with their DMP and get it signed and dated by the debtor. Every time you write to a creditor send a copy of the Letter of Authorisation with your covering letter.

Legal Action From a Debt Collector

Despite all your efforts, you may find that a creditor may continue to take legal action against you. This is why at the beginning I advised that you get a copy of Debt Advice Handbook from Amazon. This will give you a much clearer understanding of what a creditor is up to.

Seek Debt Advice

Finally, the debt industry can be very aggressive, sneaky, and confusing. So try to get as much information as you can, that relates to the debt situation that you are dealing with. Go onto debt help forums and seek advice. Read the Debt Advice Handbook as this is packed with useful information. If you think an IVA may be a solution, then read this post first: IVA’s Good or Bad? Yes a DIY DMP is tricky, but it can be done.

If you have any problems with the spreadsheet, let me know and I will see if I can rectify it.

Can I do my Own Debt Management Plan?

Yes, there is no reason why you can not do your own debt management plan. Doing your own debt management plan is not easy, if you are easily intimidated by creditors. However if you feel that doing your own debt management plan is the right thing for you, then all the information is contained within this blog.

Additional Debt Information

I would recommend the Debt Advice Handbook from the Deals and Offers section above. This book will give you a greater insight of what the creditors, bailiffs and collection agencies may do:

|

How to Get Out of Debt is an eight-stage strategy that enables readers to pay off debt and fix their finances for good. This book has it all covered. | |

|

How to Live for Free - I have done a full review on the book here: How to Live for Free | |

|

The Money Diet - revised and updated: The ultimate guide to shedding pounds off your bills and saving money on everything! | |

|

Pay Off Your Debt Book: Your Ultimate Financial Planner and Budget Companion for Managing Money Discover the Essential Debt Management and Budgeting Tool for Financial Success | |

Pingback:Wescot Debt Collection Accept £1 per Month in DMP

Pingback:Sickness Dealing with Debt

Pingback:Judgment for Claimant – What Next? – Johnny Debt

Pingback:In Debt, What should I Do? – Johnny Debt

Pingback:A Cry For Help – Debt Help Needed – Johnny Debt